On Saturday 10th October TED hosted a series of online climate change talks by global influencers and leaders, along with various panels where participants could challenge and question business leaders and others. The talks are well worth watching and are notable in the strong sense of urgency that emerges, but particularly related to the call for a reduction in global emissions of 50% by 2030. As speaker after speaker noted, this is the essential task to be achieved in the coming decade.

The call for a very sharp reduction in emissions in a short space of time emerges from the details of the IPCC Special report on 1.5°C. In that report, the authors created a series of pathways that met the stringent requirements of the carbon budgets they had established (420 GtCO2 from 1.1.2018, Table 2.2 of the main report). In the Summary for Policy Makers the authors note as follows;

C. Emission Pathways and System Transitions Consistent with 1.5°C Global Warming

C1. In model pathways with no or limited overshoot of 1.5°C, global net anthropogenic CO2 emissions decline by about 45% from 2010 levels by 2030 (40–60% interquartile range), reaching net zero around 2050 (2045–2055 interquartile range). For limiting global warming to below 2°C CO2 emissions are projected to decline by about 20% by 2030 in most pathways (10–30% interquartile range) and reach net zero around 2075 (2065–2080 interquartile range).

The carbon budget of 420 GtCO2 noted above is very limited, given that in 2018 and 2019 emissions were around 41 Gt, with 34 Gt from the use of coal, oil and gas, 2 Gt from limestone calcination for cement and about 5 Gt from land use change. So by the start of 2020 that budget had effectively fallen to 338 GtCO2. Some simple area under the curve geometry shows the need for at least a 50% reduction in emissions by 2030 to meet this. If emissions are 20 Gt in 2030, then over the decade 2020-2030 the cumulative emissions would be about 300 GtCO2, leaving precious little budget for the future years if 1.5°C is to be met without overshoot (overshoot meaning that we emit more than 420 GtCO2, possibly driving the temperature rise above 1.5°C, but then clawing this back again with removals later in the century).

As has been noted by many observers, the COVID-19 pandemic has helped with emission reduction in 2020, but it has yet to give rise to structural change that could see emissions continue to fall sharply. In the Shell Rethinking the 2020s scenarios released recently, structural change does start to emerge in the Health First story line, but not enough for a 50% reduction by 2030. None of the scenarios show that scale of change.

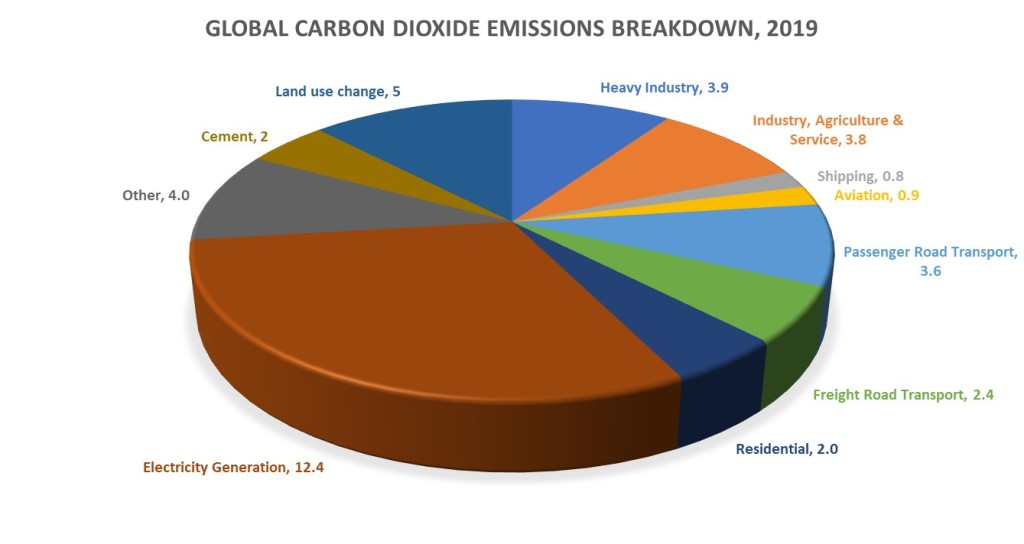

But if emissions were to fall by 50% by 2030, i.e. to 20 Gt, then what might that look like? In just a decade the global energy system would need to look very different. Starting with current carbon dioxide emissions, the breakdown going into 2020 is approximately along the following lines;

Within the breakdown, there are changes that can be made and changes that are unlikely. This isn’t just a case of every sector and every activity reducing by 50%. Some may even grow just to force reductions in others! Notably;

| Sector | Discussion | Required or Expected Outcome (Gt) |

| Electricity generation | Clear commercial alternatives to gas and coal are now available, so an accelerated transition should be possible. But given its size and current emissions, this is the sector that has to do the early heavy lifting in terms of emission reductions. | 3.0 |

| Residential | Primarily natural gas, heating oil and LPG in homes, which may be slow to dislodge. However, in a decade nearly half of all households may have to replace boilers and incentives could be applied to force a change to electricity for cooking. | 1.0 |

| Freight road transport | This is unlikely to change in the short term due to the lack of a clear alternative technology. Hydrogen fuel cell trucks will only make an impact in the 2030s and beyond. | 2.5 |

| Passenger road transport | Change is now possible in this sector, but EV manufacture would have to be ramped up very rapidly. | 1.0 |

| Aviation | The only major change possible in the short term is a reduction in use rather than actual mitigation. The pandemic may ensure this happens, but if not, society will have to make difficult choices. | 0.5 |

| Shipping | This may increase in the short term due to the quantity of materials needed to move throughout the world to rebuild the power generation sector and manufacture batteries. A new generation of ships won’t appear until the 2030s. | 1 |

| Industry, agriculture and services | This may increase in the short term due to the quantity of materials needed to be produced throughout the world to rebuild the power generation sector and manufacture batteries. However, a shift to further electricity use might be able to counter this trend. | 3.5 |

| Heavy industry | This will almost certainly increase in the short term due to the quantity of materials needed to be mined and processed throughout the world to rebuild the power generation sector and manufacture batteries. New low emission processing technologies won’t be in place within a decade. | 4.5 |

| Land use change | Government policy applied rigorously throughout the world ought to be able to end deforestation within a decade, given sufficient impetus and attention. | 0 |

| Cement | This will hardly change in a decade despite efforts to reduce emissions at a facility level given the quantity of cement required for wind turbine foundations and other construction needs within the transition. | 2 |

| Other | This category of emissions is largely related to the energy use in processing and delivery of fossil fuels to market. As fossil fuel use declines in this story, this category should decline proportionately. | 2 |

| Total across all sectors | 21.0 |

The above table isn’t a forecast or scenario, but an indicative picture of what would have to happen to achieve a near 50% reduction in global emissions, taking into account some practical considerations. The 2020s reduction effort falls on three main sectors; electricity generation, passenger vehicles and ending deforestation. That doesn’t mean no changes elsewhere, they just won’t be very visible by 2030 although significant efforts will have to be made to prepare a range of industrial and transport technologies for deployment in the 2030s.

Electricity Generation – The world currently has 2000 GW of coal capacity, the vast majority of which would have to shut down in the 2020s, replaced by wind and solar. As grid batteries are not yet a mainstream technology for managing lengthy periods of intermittency, backup would likely come from existing natural gas facilities so as to keep emissions to a minimum. Some 8000 GW of renewable capacity might be needed (not forgetting that electricity demand will also increase because of transport demands), with solar and offshore wind overlapping in many regions to provide 24/7 coverage, with assistance from nuclear and hydro where available and natural gas when necessary. In 2019 the world had 600 GW each of solar and wind, generating about 800 TWh and 1500 TWh, or 8-9% of global electricity demand. Capacity increased by 100 GW solar and 60 GW wind between 2018 and 2019, so this would need to increase by about 30% per annum year on year throughout the 2020s. It means that by 2030, the global solar capacity build rate would need to be around 1000 GW per year, ten times that of today.

Passenger Vehicles – Today, global battery electric vehicle (BEV) production is approaching 2 million per year and there are about 6-7 million BEVs on the road, compared to total vehicle manufacturing capacity of 80 million and over a billion passenger vehicles on the road. This results in 3.6 billion tonnes of carbon dioxide per year. To reduce this to 1 billion tonnes per year by 2030, some 600-700 million BEVs would need to be produced, which means a complete switch to BEV manufacture by all the major automakers before 2025. The supply chain required to feed such a shift in manufacturing would also require a rapid increase in mining activities for key battery materials such as cobalt, lithium and nickel. The expansion of existing mines, the opening of new mines and the construction of sufficient processing facilities to refine the ores would all need to be complete by 2024, which means an almost immediate and sharp ramp up in global activity, well beyond that currently underway for the already planned battery factories.

Ending deforestation – This task is both the easiest and most difficult at the same time, in that the decision to chop down a tree is an entirely human impulse based on the need to do something different with the land. It is entirely possible for everyone to decide to stop deforestation, but hardly plausible that they will. Deforestation is closely linked with human development, the provision of food and growing populations. Ending deforestation in a decade also means meeting the UN Sustainable Development Goals, in that achieving these would remove much of the need to deforest additional land.

As noted in the table above, there are other sectors that must take action, but some time must be allowed for technologies to permeate and become deployable. For example, hydrogen may play a role decarbonising heavy freight vehicles through fuel cell technology, but no such truck currently exists as a commercial proposition. By the late 2020s such trucks will likely exist, but the number on the road by 2030 will still be small.

In addition to all the above, the emissions of other gases will need to fall. Methane emissions should come down globally as the oil and gas industry contracts in this scenario, but something will also have to happen with agricultural methane. That probably points to diet change – notably a shift away from red meat towards chicken, pork and plants. Such a move would also help with the deforestation task.

Achieving all of the above in a decade may not be possible, or it could perhaps happen through a combination of the above and a broad cessation of emission intensive activities and consumerism by much of the global population. As it stands today, there is not a single national policy framework in operation today that is aimed at delivering such a change. Irrespective, this illustration is not meant to challenge the proposition, only outline what it means and quickly build understanding. That perhaps is the first step to actually doing it.

Average Rating